The data center is as tight as a drum. DRAM main memory and flash memory prices are going crazy as hyperscalers, cloud builders, and AI model builders try to get heavy configurations to boost the performance of their expensive GPUs and XPUs. Which have mostly been allocated for the whole of 2026, just like Intel and AMD processors as well as the local population.

HBM memory capacity, which is vital for most AI accelerators, has likely been largely allocated, although one could argue that Micron Technology, Samsung, and SK Hynix have very little incentive to lock in HBM prices now for future sales because, just like DRAM and flash, every time someone looks, the price goes up.

My advice is to stop looking. . . .

Likewise, demand for chip etching and packaging from the world’s largest, most advanced and most consistent foundry is outstripping supply, giving Taiwan Semiconductor Manufacturing Co great control over its prices. But even with Intel trying to bring its foundry together – and there are indications that it is doing so – and Samsung getting better and better every year at making chips for others in its foundry, TSMC doesn’t really have much competitive pressure.

The company can go out of business if it wants (we’re not saying it does, but it certainly should focus on the most profitable deals it can do), and the incremental revenue it can extract from its smelters in Taiwan, the US, China and Japan continues to increase each quarter.

And the number of etched wafers it can produce each month has finally emerged from the doldrums of 2023 and 2024. So revenues are growing and the bottom line is growing faster, as it has been since the third quarter of 2024, when GenAI’s boom shifted from chemical to nuclear.

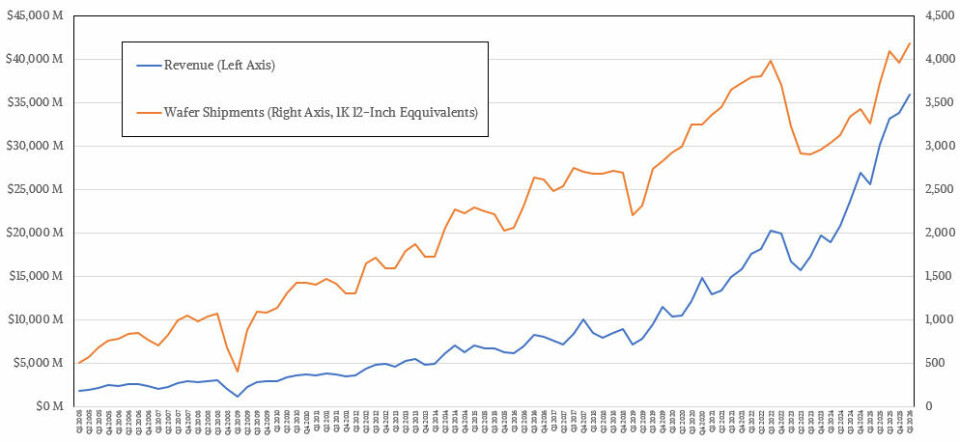

Measured in 12-inch (300 mm) wafer equivalents across all of its machines and in all of the many process nodes in which TSMC still etches chips, the foundry manufactured 4.17 million wafers in the 2026 quarter, which was a record for the company, even surpassing the 4.09 million wafers it produced in the third quarter of 2025. That wafer rate in the March quarter was 28.1%. higher than that of the year. a period ago and up 5.4 percent sequentially. Of course, chips come in all shapes and sizes, with dozens or even hundreds per wafer, so it’s hard to get a sense of how many chips TSMC produces, but it surely knows that number and tracks it very carefully as well.

Revenue per wafer is also growing, suggesting a more complex chip and the significant packaging involved in getting a high-end chip made by TSMC. Only four years ago, TSMC averaged less than $5,000 in revenue per wafer (that is, total revenue divided by 12-inch equivalent wafer production), but in the March quarter, revenue per wafer increased 1.7 times from four years ago, to $8,600. This revenue per wafer increased 9.8% year-over-year from the $7,832 level set in Q1 2025, but only increased 1% sequentially.

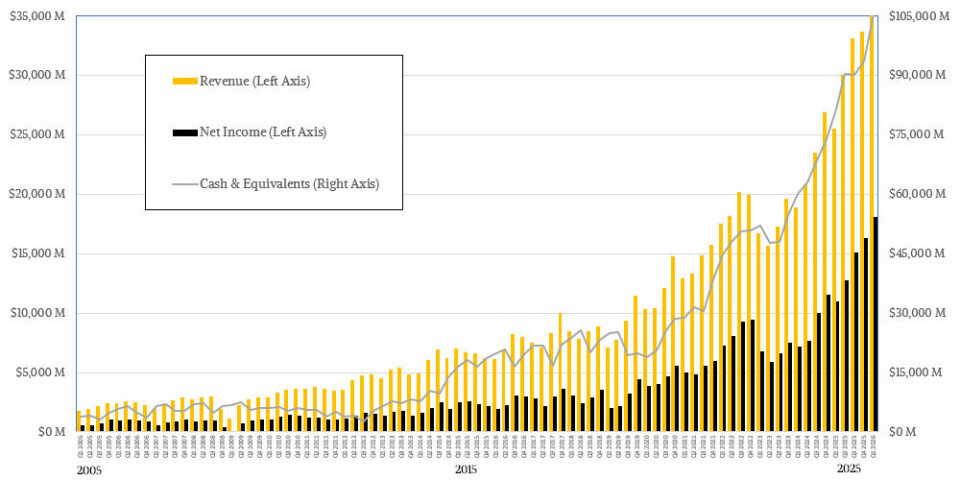

Add in all those wafers and packaging, and TSMC reported sales of $35.9 billion, up 40.6% year over year in the March quarter, and net income exploded 65.2% to $18.13 billion, representing a crazy 50.5% of revenue. TSMC is a highly complex, capital-intensive hardware maker with margins that rival any software stack in history, including the venerable IBM mainframe that still keeps the company afloat due to the inflexibility of applications written over decades on the System/360 and its descendants.

TSMC ended the quarter with $105.53 billion in cash and equivalents in the bank thanks to those booming profits, and it only plans to spend between $52 billion and $56 billion on capital spending in 2026. In its call with Wall Street analysts, TSMC just raised that number to the “high end” of that range. So call it $56 billion. Capital spending will undoubtedly increase in the coming year and beyond, but it’s convenient that TSMC has nearly two years of investment in the bank and it’s only the beginning of the current year.

But what does that amount of money actually buy? TSMC says between 70% and 80% of this year’s investments will be in foundries, meaning a mix of expansion of the N3 node (3 nanometers), construction of the N2 node (2 nanometers) and the start of the A14 node (1.4 nanometers) in Taiwan, as well as the continued ramp-up of foundry operations started a few years ago in Arizona. Depending on who you ask, for fabrication modules capable of handling 50,000 wafer starts per month, a 3-nanometer fabrication module costs about $20 billion, a 3-nanometer module costs about $28 billion, and a 1.4-nanometer module costs on the order of $49 billion. Instead of moving to High NA processes, which will cut the reticle size in half but radically increase transistor density, TSMC is doing a lot of extra modeling with its N2 and A14 processes, which means more equipment but fewer problems and changes for customers.

TSMC’s total capacity in 2025 in terms of wafer starts per month “exceeded 17 million 12-inch wafer equivalents,” which was quite a bit higher than the level set in 2024. TSMC is going to have another growth spurt, of course, but will not and cannot add that much capacity to not be able to charge the scarcity premium it enjoyed in 2025 and 2026 and beyond.

To be precise: even if TSMC could move much faster, given the state of the global economy and the concentration of GenAI spending among tech titans, it wouldn’t. There’s very little upside for TSMC in creating its own recession cycle – especially after experiencing one when spending on PCs, smartphones and general purpose servers all went off the rails in 2022 and 2023.

TSMC has always talked about its business in terms of revenue per platform and revenue per process node, and we’ll take a quick look at those. But what everyone wants to know is how focused TSMC’s business is on chips for computing and AI networks, and that’s something the company is only hinting at. We tried to estimate it based on the lack of statements from TSMC in recent quarters.

First, revenue by process:

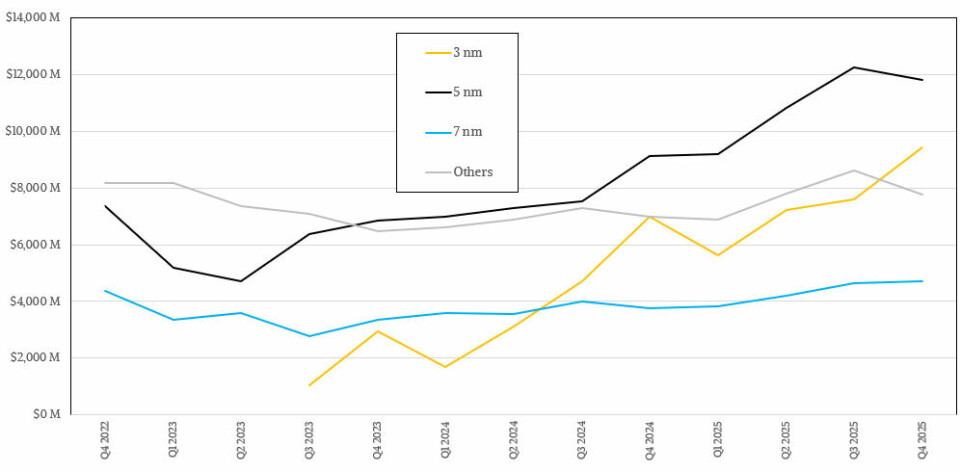

Volume production of the N5 process began almost six years ago, and it is still the dominant manufacturing process (along with its N4 variants) in the TSMC fleet, at least judging by revenue, which was $12.92 billion in the first quarter, up 40.6% year-over-year and 9.5% sequentially. The N5/N4 node certainly does not appear to have reached its peak. These are relatively low-cost, high-efficiency manufacturing nodes, and many chip companies remain behind for precisely these reasons. Nvidia and AMD can pay for cutting-edge nodes because they can charge a lot of money for CPUs and GPUs.

The N3 node, a few years younger, is finding its feet, with revenue of just under $9 billion in the first quarter of 2026, up 59.8% but down 5% sequentially. The much older N7 node (along with its N6 variant) is not only booming, but growing, with sales up 21.9% to $4.67 billion. All other nodes – and there are plenty of older products made around the world – accounted for $9.33 billion in sales and grew 35.4% in the March quarter. This type of revenue is what the old Intel foundry model moved away from, year after year, because it had a captive, cutting-edge customer and was not a merchant foundry. Intel would kill for a company this old, and one day it might even build it.

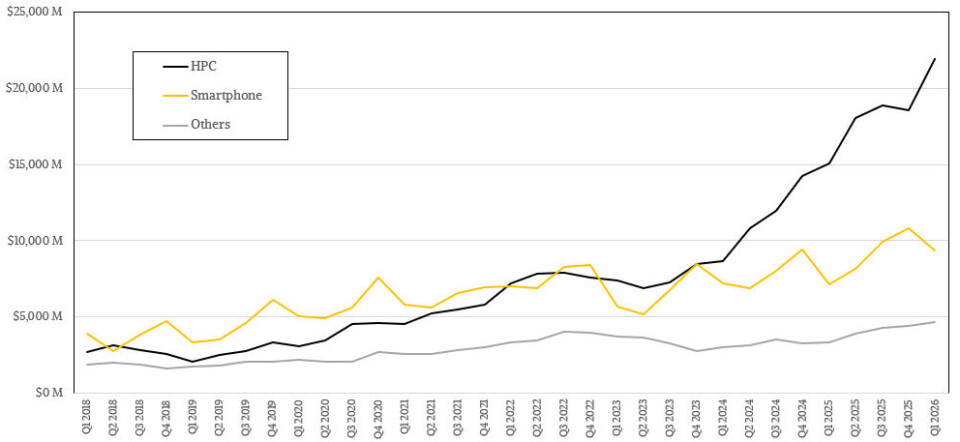

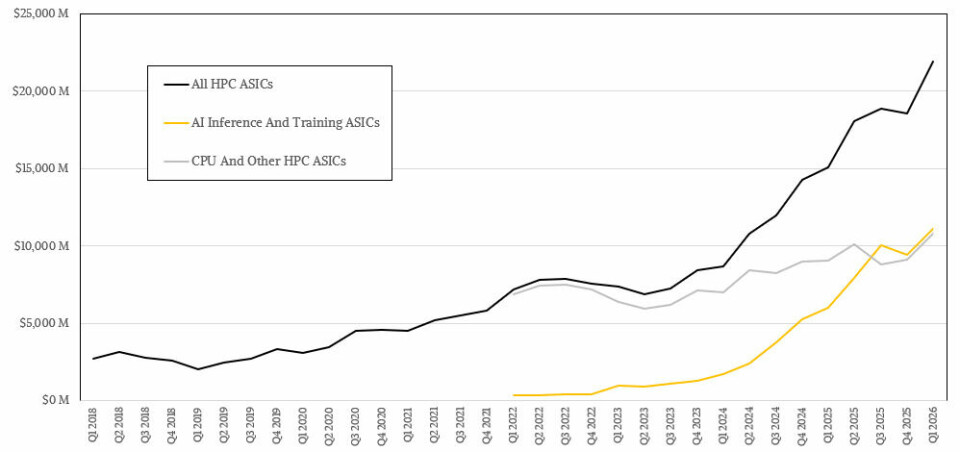

With the revenue breakdown by product, we can start to zoom in on the AI part of the action at TSMC. As always, we need to be careful with the terms here. When TSMC says HPC, it means all types of high-performance chips, which include processors used in PCs and servers, GPUs and XPUs, various types of switching and routing ASICs, and FPGAs.

It has been nine quarters since TSMC’s HPC segment tied with the smartphone segment in terms of revenue generated. Now, the HPC segment, which recorded $21.9 billion in sales in the first quarter of 2026, is more than twice as large as the smartphone segment, which had $9.33 billion in sales. As you can see, the HPC segment is growing faster, up 45.4% year-over-year and 18% sequentially – and I don’t think all of this growth is driven by AI.

Many high-end PC and server processors are manufactured these days and are also sold out. Even though the smartphone chip sector has seen a very healthy growth of 30.6%, unless the GenAI bubble bursts, I don’t think smartphones will ever be able to catch up to HPC at TSMC. It’s much more likely that TSMC will divide HPC into AI and non-AI segments, as this is actually an important distinction that investors deserve to know.

Which brings us to this pretty little painting:

There’s a lot of witchcraft in this one, make no mistake, but our model is consistent with the long-term compound annual growth rate that TSMC has pegged at “mid to high 50%” between 2024 and 2029. That forecast was for an average CAGR of 40% in early 2025.

I said that eventually the GenAI boom would stop growing explosively, but it would continue to grow very quickly and become very large. And our model reflects this belief because it is the curve that new and explosive technologies follow. Additionally, TSMC’s revenue depends much more on supply than demand, and like I said, it can’t overbuild its capacity even if it wanted to. And TSMC certainly doesn’t want to do that.

In 2022, we think TSMC’s AI business was just $1.52 billion, but it grew triple-digit quarterly through much of 2023, 2024, and the first three quarters of 2025 to reach a staggering $33.38 billion for all of 2025. I think the growth rate for the fourth quarter of 2025 and the first quarter 2026 was much slower, 79% and 84.9 percent year-over-year, respectively. But in those two quarters, the AI chip business generated just over half of TSMC’s overall HPC chip revenue, and by the next quarter it will likely account for more than a third of TSMC’s overall revenue. (And I’m not counting PC AI processors in that number, nor are I counting processors with matrix or vector engines. They can do AI in parallel, but that’s not their primary focus.)

To give some numbers, I think the non-AI part of the TSMC HPC business generated about $10.8 billion, up 19.2%, and the AI part generated about $11.1 billion, up 84.9%.

That’s pretty surprising for a company that was interesting but not overwhelming just four years ago.